Owning a rental property offers financial opportunities, but it also comes with tax obligations. Whether you’re new to real estate or expanding your portfolio, accurately reporting earnings is essential. At Whetzel Homes Collective in St. George, Utah, we simplify these complexities with actionable insights tailored to investors like you.

All earnings from leased properties must be reported to the IRS using Schedule E (Form 1040). This includes advance payments, security deposits retained due to lease violations, and even non-refundable fees. Deductions for ordinary expenses—like maintenance, mortgage interest, and property management fees—can significantly reduce your taxable amount.

Depreciation is another critical factor. Residential properties depreciate over 27.5 years, spreading the cost of the asset across its useful life. However, distinguishing between repairs (immediately deductible) and improvements (depreciated over time) requires careful attention. Our team at (435) 334-1544 helps clients navigate these nuances to optimize their returns.

Key Takeaways

- Earnings from leased properties must be reported on Schedule E (Form 1040).

- Depreciation for residential buildings spans 27.5 years under IRS guidelines.

- Security deposits may become taxable if withheld for damages or unpaid rent.

- Differentiate between deductible repairs and depreciable improvements.

- Ordinary expenses like maintenance and mortgage interest lower taxable amounts.

Introduction to Rental Income and Tax Basics

Generating earnings through property leasing involves specific tax responsibilities. The IRS defines taxable earnings as any payment received for the use or occupation of real estate. This includes monthly lease payments, non-refundable fees, and retained security deposits. Properly categorizing these amounts ensures compliance and avoids penalties.

Managing income expenses plays a pivotal role in reducing taxable amounts. Landlords can deduct costs like maintenance, insurance, and utilities directly tied to their properties. However, personal expenses unrelated to leasing activities—such as home renovations for private use—are not eligible.

| Expense Type | Examples | Tax Treatment |

|---|---|---|

| Deductible | Repairs, advertising, HOA fees | Subtracted from taxable earnings |

| Non-Deductible | Principal mortgage payments, personal travel | Not eligible for deductions |

| Property Taxes | County assessments | Fully deductible annually |

Property taxes directly influence annual liabilities. These levies are deductible in the year they’re paid, offering immediate relief. For owners of multiple rental properties, tracking location-specific rates becomes critical to avoid overpayment.

All earnings and deductions must be reported on Form 1040, specifically Schedule E. Unlike wages or business income, leasing revenue requires separate documentation to account for depreciation and passive activity rules. Whetzel Homes Collective assists clients in St. George, Utah, with these fundamentals—call (435) 334-1544 for personalized guidance.

How Rental Income Is Taxed

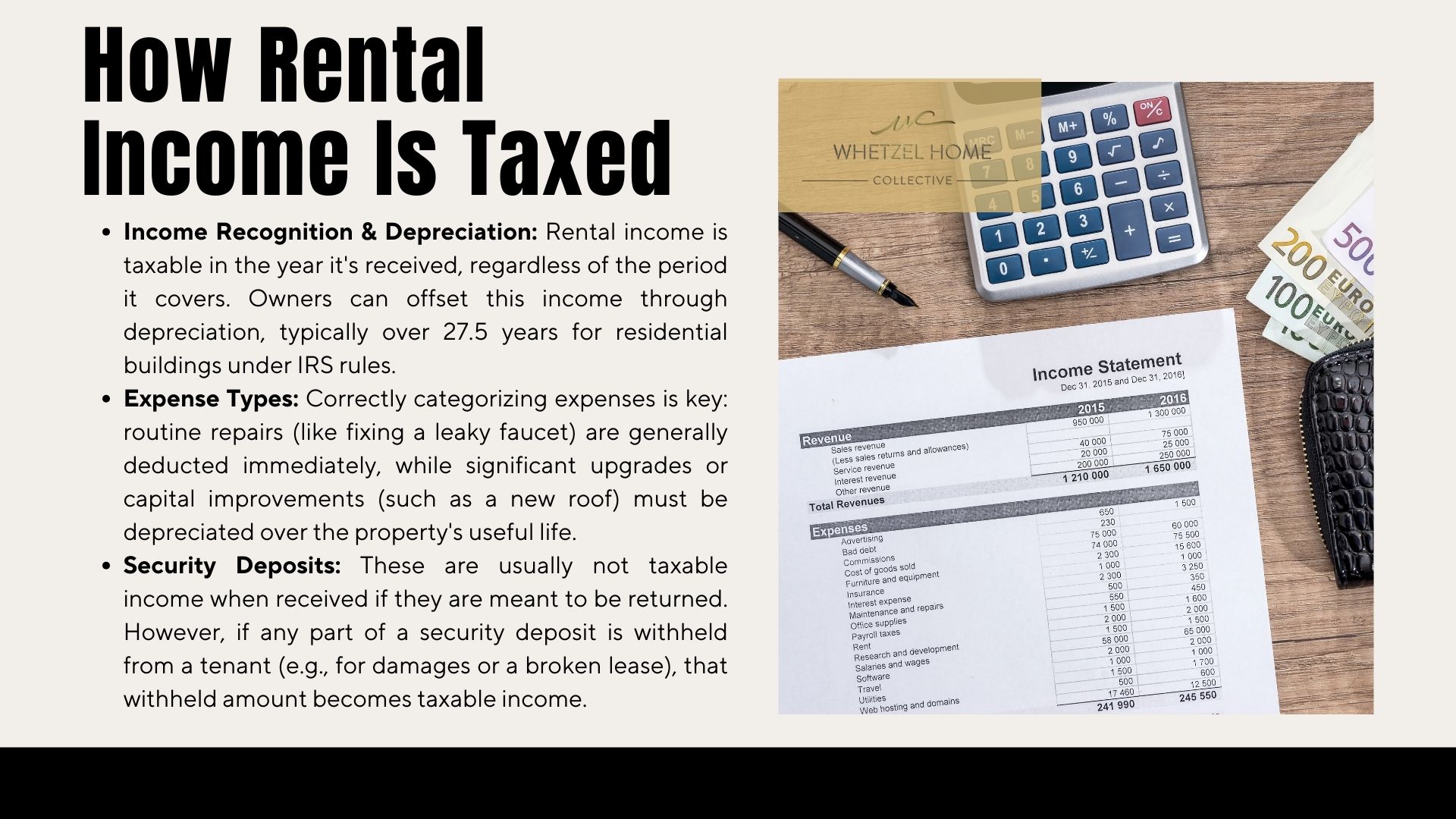

Real estate investors must align financial practices with IRS regulations to optimize returns. Earnings from leased assets become taxable in the year they’re received, even if payments cover future periods. For example, a tenant paying January’s payment in December requires reporting that amount as part of the current year’s earnings.

Depreciation offers a strategic way to offset earnings over time. Residential buildings follow a 27.5-year schedule under IRS guidelines, spreading deductions across nearly three decades. This reduces taxable amounts while accounting for wear and tear.

Correctly categorizing expenses ensures maximum savings. Repairs like fixing a leaky faucet can be written off immediately. Upgrades such as installing a new roof must depreciate alongside the property’s 27.5-year timeline.

Security deposits typically aren’t taxable unless withheld. If a tenant breaks their lease and forfeits part of their deposit, that amount becomes reportable. Tracking these scenarios helps avoid discrepancies during filing.

At Whetzel Homes Collective in St. George, Utah, we clarify IRS rules for property owners. Whether managing advance payments or depreciation schedules, our team ensures compliance. Call (435) 334-1544 to streamline your tax strategy today.

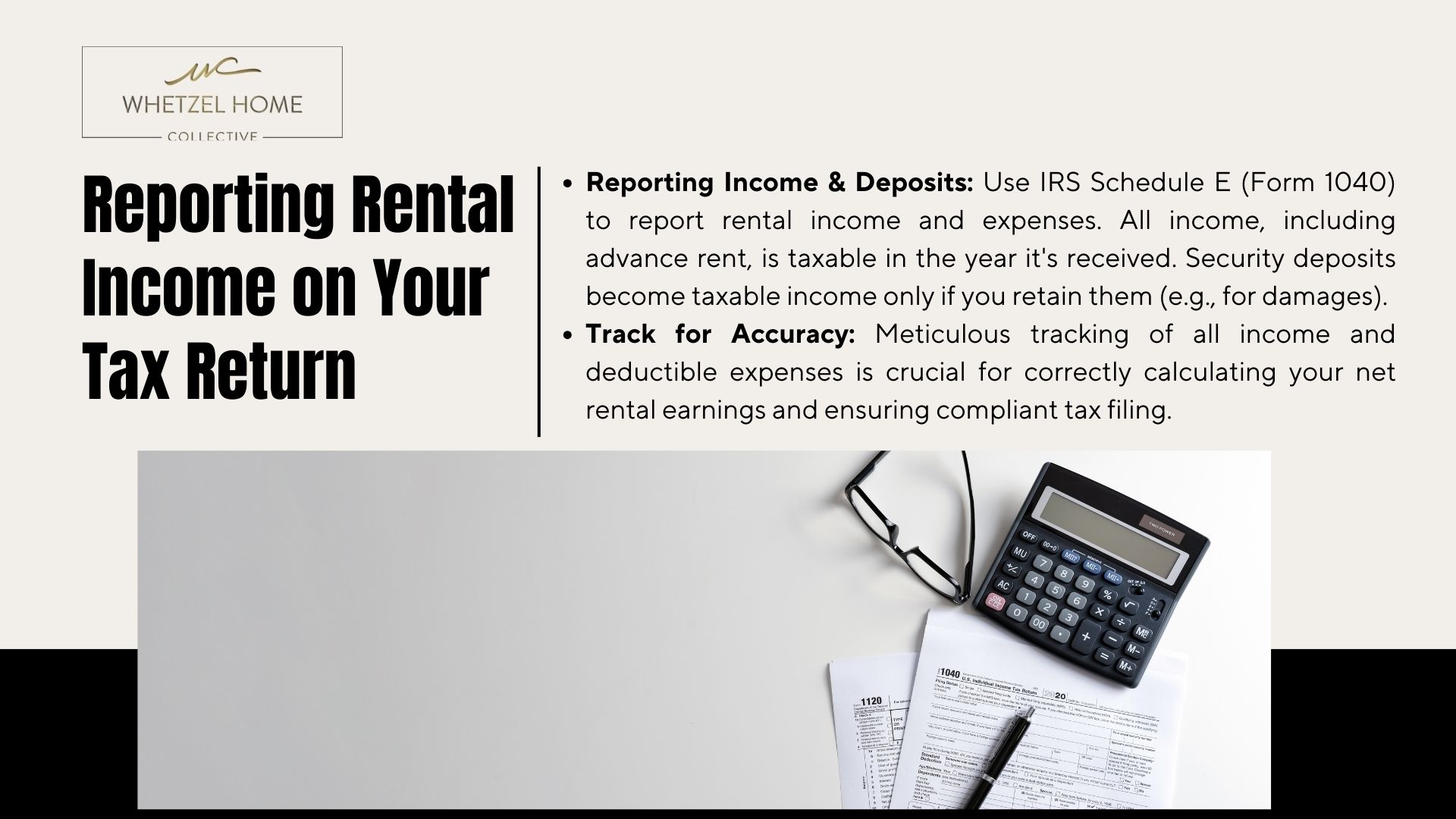

Reporting Rental Income on Your Tax Return

Accurate reporting forms the backbone of compliant property management. Schedule E (Form 1040) serves as the IRS’s primary tool for declaring earnings and expenses tied to leased assets. Whetzel Homes Collective simplifies this process through organized templates that align with federal requirements.

Schedule E: Supplemental Income and Loss

This form captures all revenue streams, including monthly payments and non-refundable fees. For example, if a tenant pays $1,200 in December for January occupancy, report it in the current tax year. Expenses like repairs and insurance premiums offset taxable amounts line by line.

Documenting Deposits and Advance Rent Payments

Security deposits require careful tracking. Refundable amounts aren’t taxable unless retained for damages. Advance payments for future months count as earnings when received. Clear records prevent misclassification during filing.

| Payment Type | Tax Treatment | Example |

|---|---|---|

| Refundable Deposit | Non-taxable unless withheld | $500 security deposit returned in full |

| Advance Rent | Taxable upon receipt | $1,500 payment for next month’s lease |

| Damage Withholding | Taxable as earnings | $300 deducted for wall repairs |

A landlord collecting $12,000 annually with $3,500 in deductible expenses would report $8,500 as net earnings. Meticulous expense tracking—using tools like digital receipts or property management software—ensures accuracy. St. George investors can call Whetzel Homes Collective at (435) 334-1544 for tailored reporting strategies.

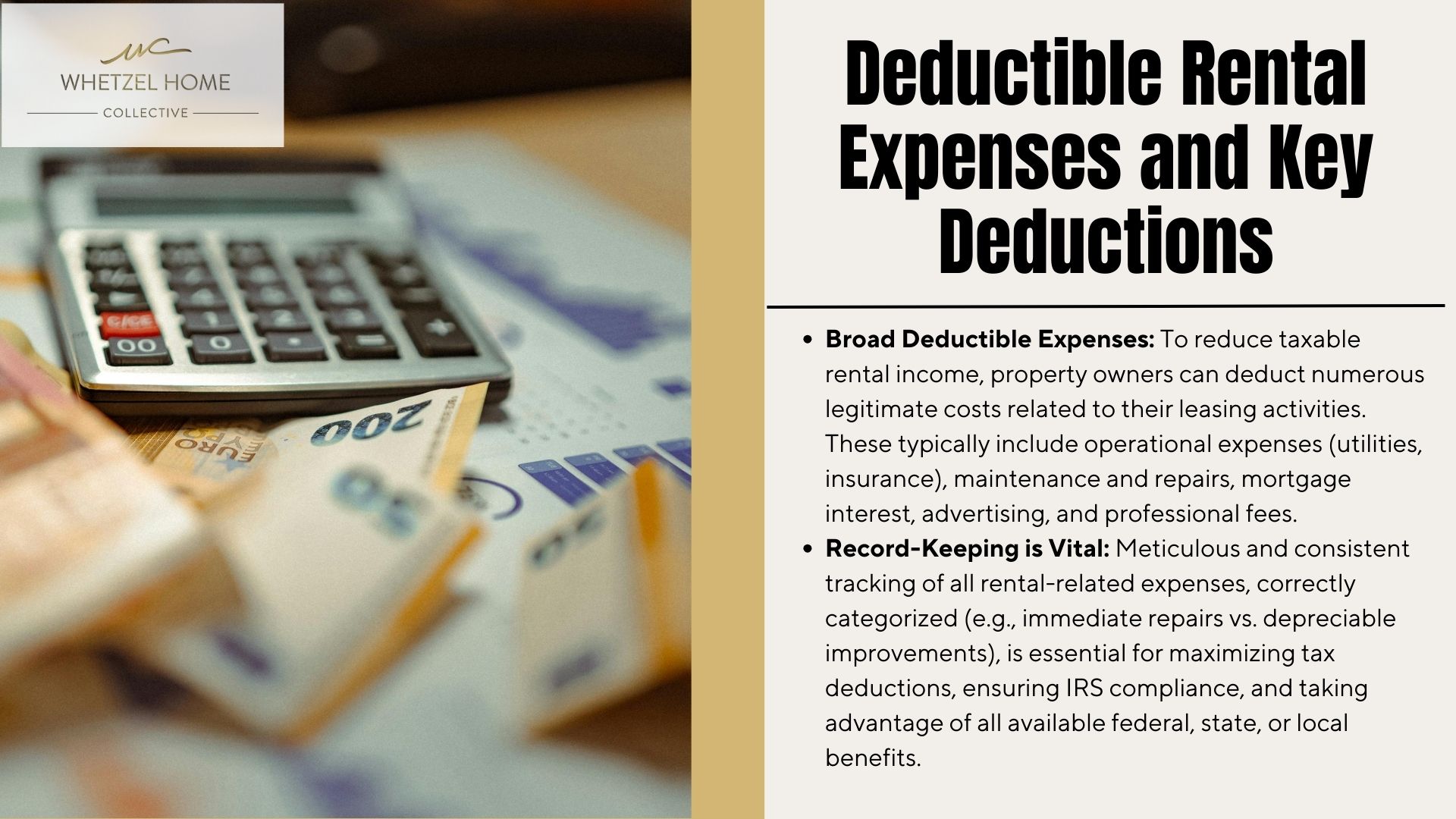

Deductible Rental Expenses and Key Deductions

Maximizing tax savings requires understanding which costs qualify as deductible. Property owners can reduce taxable earnings by claiming legitimate expenses tied to leasing activities. Proper categorization and documentation ensure compliance while unlocking financial benefits.

Common Deductible Expenses

IRS guidelines allow deductions for costs directly related to property operations. These include routine upkeep, insurance premiums, and fees paid to professionals. For example:

- Advertising vacancies on local platforms

- Repairing broken appliances or plumbing

- Paying property management companies

| Category | Examples | Federal Eligibility |

|---|---|---|

| Operational | Utilities, HOA fees | Fully deductible |

| Maintenance | Landscaping, pest control | Immediate write-off |

| Financial | Mortgage interest, loan fees | Annual deduction |

Tax Benefits and Expense Tracking

Detailed records transform everyday costs into tax-saving opportunities. A landlord who spends $5,000 annually on repairs could lower taxable earnings by that amount. State-specific rules may offer additional savings—Utah, for instance, permits deductions for energy-efficient upgrades.

Whetzel Homes Collective recommends using digital tools like QuickBooks or Stessa to track transactions. One client reduced liabilities by $2,400 simply by documenting mileage for property visits. As tax expert Jane Miller notes:

“Consistent record-keeping turns overlooked receipts into actionable deductions.”

Blending federal guidelines with local requirements maximizes returns. Our St. George team helps investors implement tailored systems—call (435) 334-1544 to refine your strategy today.

Calculating Rental Property Depreciation

Depreciation transforms property investments into long-term tax advantages. By spreading costs over decades, investors lower annual liabilities while maintaining asset value. Whetzel Homes Collective emphasizes mastering this process to unlock consistent savings.

Determining Your Cost Basis

Start by calculating your property’s cost basis. This includes the purchase price, closing costs, and qualifying improvements. Subtract the land value—since it doesn’t depreciate—to focus on the building’s worth.

For example, a $300,000 purchase with $50,000 allocated to land creates a $250,000 depreciable basis. Upgrades like roof replacements add to this figure, while routine repairs don’t.

Depreciation Methods and Schedules

Residential buildings typically use the straight-line method over 27.5 years. Commercial properties often follow a 39-year schedule. Components like appliances depreciate faster—usually 5 years.

| Asset Type | Depreciation Period | Annual Deduction |

|---|---|---|

| Residential Building | 27.5 years | $9,091 ($250,000 basis) |

| Appliances | 5 years | $2,000 ($10,000 value) |

| Landscaping | 15 years | $667 ($10,000 investment) |

Using Form 4562 ensures proper IRS reporting. One St. George investor reduced taxable amounts by $11,758 annually through strategic depreciation planning. As our team advises:

“Accurate asset classification turns depreciation from a paperwork task into a wealth-building tool.”

Whetzel Homes Collective simplifies these calculations for Utah property owners. Call (435) 334-1544 to align your strategy with IRS standards.

Differentiating Improvements Versus Repairs

Property owners often face confusion when categorizing expenses tied to their assets. Proper classification impacts tax savings and long-term financial planning. Let’s break down the IRS guidelines to clarify this critical distinction.

Recognizing Capital Improvements

Capital improvements enhance a property’s value or extend its lifespan. These upgrades must be depreciated over time rather than deducted immediately. Examples include installing energy-efficient windows or replacing an entire HVAC system.

Identifying Routine Repairs

Routine repairs maintain a property’s current condition without adding significant value. Fixing a broken door handle or repainting walls between tenants typically qualifies. These costs can be written off in the year they occur.

| Expense Type | Examples | Tax Treatment |

|---|---|---|

| Capital Improvement | New roof, room addition | Depreciated over 27.5 years |

| Routine Repair | Plumbing fixes, patching drywall | Full deduction in current year |

Management decisions directly affect expense classification. A Whetzel Homes Collective client upgraded kitchen cabinets but later realized partial costs qualified as repairs. By splitting the project into “replacements” (improvements) and “cosmetic updates” (repairs), they optimized deductions.

Accurate tracking saves time and maximizes deductions. For example, replacing a water heater adds value and follows a depreciation schedule. Repairing a leaky unit simply maintains functionality. As tax strategist Laura Whetzel advises:

“Treat every expense like a puzzle piece – proper placement reveals the full financial picture.”

Understanding these rules helps streamline payments and avoid IRS disputes. Schedule a consultation at (435) 334-1544 to refine your expense management strategy today.

Understanding Passive Activity and Active Participation

Navigating IRS classifications for property management can significantly impact your tax outcomes. Most leasing activities fall under passive activity, limiting how losses offset other earnings. However, meeting specific criteria for active involvement unlocks exceptions.

Passive Loss Rules Explained

The IRS restricts passive losses from offsetting non-passive earnings like wages. For example, a $5,000 annual loss on a property can’t reduce your salary taxes unless you qualify as an active participant. Exceptions apply if your modified adjusted gross income stays below $100,000.

Requirements for Active Participation

To claim this status, you must make key management decisions, such as approving tenants or setting lease rates. The IRS also requires at least 10% ownership and 500 hours of annual involvement. Property management services can count toward this threshold if you oversee their work.

| Criteria | Minimum Requirement | Impact on Deductions |

|---|---|---|

| Ownership Stake | 10% or more | Enables loss deductions |

| Decision-Making | Approving contracts, repairs | Supports active status |

| Annual Hours | 500+ (direct or supervised) | Qualifies for exceptions |

Management fees and third-party services remain deductible, but they don’t automatically satisfy participation rules. As Laura Whetzel of Whetzel Homes Collective advises:

“Track time spent reviewing invoices or coordinating repairs—these details prove active engagement during audits.”

Strategic planning enhances your property’s long-term value while complying with IRS standards. Our team in St. George simplifies these guidelines—call (435) 334-1544 to align your strategy.

Strategies for Reducing Tax Liability on Rental Income

Smart financial planning can transform property ownership into a tax-efficient venture. By combining federal guidelines with localized strategies, landlords significantly lower annual obligations while maintaining compliance.

Maximizing Deductions and Credits

Every dollar spent on qualifying expenses reduces taxable amounts. Common opportunities include:

- Claiming insurance premiums for property coverage

- Writing off travel costs for maintenance visits

- Utilizing energy-efficiency credits for solar installations

One St. George investor saved $4,200 annually by documenting mileage for tenant meetings. Utah offers a 5% tax credit for storm-resistant upgrades—a benefit often overlooked.

State-Specific Opportunities

Tax rules vary widely across jurisdictions. Texas exempts property taxes for senior tenants, while California allows accelerated depreciation for earthquake retrofits. Key considerations:

- Local homestead exemptions

- Rent control ordinance impacts

- Disaster relief provisions

Whetzel Homes Collective helped a client in Hurricane, Utah, reduce liabilities by 18% through strategic lease structuring. As tax advisor Mark Thompson notes:

“State-specific savings often hide in plain sight—partnering with local experts reveals hidden advantages.”

Proactive expense tracking and tailored consultations ensure maximum deductions. Our team identifies opportunities like negotiating repair costs with tenants to boost deductible amounts. Call (435) 334-1544 to refine your approach today.

Utilizing Cost Segregation and 1031 Exchanges

Advanced tax strategies can unlock significant savings for property owners. Cost segregation studies accelerate depreciation by reclassifying components like appliances or landscaping. For example, a $500,000 property might allocate $150,000 to 5-year assets—boosting annual deductions by $30,000 and lowering your tax bill.

1031 exchanges defer capital gains taxes when reinvesting sale proceeds into similar properties. Selling a $750,000 asset and purchasing a $1 million replacement defers taxes on $250,000 in gains. Strict timelines apply—you must identify a new property within 45 days and close within 180.

| Strategy | Benefit | Example |

|---|---|---|

| Cost Segregation | Front-loaded deductions | $12,000 annual savings on commercial upgrades |

| 1031 Exchange | Deferred tax liability | Reinvesting $500k sale into larger multifamily unit |

| Combined Approach | Enhanced cash flow | Accelerated depreciation + tax-free equity growth |

Timing is critical. Coordinating a 1031 exchange while addressing routine maintenance ensures properties remain competitive. Mortgage interest remains deductible, but principal payments don’t qualify—plan refinancing carefully.

Whetzel Homes Collective guides clients through these complex processes. As Laura Whetzel explains:

“Strategic planning turns IRS rules into financial tools—we help investors maximize benefits while avoiding pitfalls.”

Though these methods require expertise, they transform tax bills into opportunities. Call (435) 334-1544 to explore how these strategies align with your portfolio.

Tips for Accurate Record-Keeping and Financial Management

Effective financial management starts with organized records. Property owners who maintain clear documentation simplify tax preparation and minimize audit risks. Whetzel Homes Collective recommends these proven methods to streamline your processes.

Organizing Financial Documents

Create separate folders for each property—physical or digital. Label receipts by category (repairs, utilities) and date. For leased assets, retain:

- Lease agreements and security deposit records

- Invoices for repairs and upgrades

- Bank statements showing payments received

Digital scanners like Adobe Scan convert paper receipts into searchable files. Store backups on encrypted cloud platforms for easy access during tax season.

Leveraging Accounting Tools

Software automates expense tracking and generates IRS-ready reports. Popular options include:

| Tool | Features | Best For |

|---|---|---|

| QuickBooks | Automatic mileage tracking | Multi-property portfolios |

| Stessa | Depreciation schedules | New investors |

| Expensify | Receipt matching | Mobile users |

Set monthly reminders to reconcile accounts. Categorize transactions as they occur—delayed entries increase errors. As Laura Whetzel advises:

“Treat record-keeping like brushing teeth—daily attention prevents major issues later.”

St. George property owners can schedule consultations at (435) 334-1544 for personalized systems. Proactive documentation turns tax season from stressful to strategic.

Conclusion

Mastering property taxation unlocks financial potential while ensuring compliance. Strategic use of property tax deductions and tracking rental income expenses helps lower annual obligations. Accurate reporting on your tax return remains essential—every documented repair or improvement impacts your bottom line.

Organized records and proactive planning simplify complex processes. Advanced strategies like depreciation schedules or cost segregation studies amplify savings over time. These tools transform IRS guidelines into opportunities for growth.

Whetzel Homes Collective in St. George, Utah, provides tailored guidance for property owners. Our team clarifies deductions, documentation standards, and state-specific rules to optimize your outcomes.

Ready to streamline your approach? Call (435) 334-1544 today. Let’s turn informed decisions into lasting financial success together.

FAQ

What counts as taxable earnings from properties?

Taxable earnings include monthly lease payments, non-refundable deposits, fees for lease cancellations, and payments received for covering a tenant’s expenses (e.g., repairs). Refundable security deposits are excluded unless retained.

Are security deposits considered taxable?

Refundable deposits aren’t taxed unless kept due to lease violations. Non-refundable deposits (e.g., pet fees) and advance rent payments are taxed in the year they’re received.

Where do I report earnings and expenses on tax forms?

Use IRS Schedule E (Form 1040) to declare revenue, deductible costs, and depreciation. This form consolidates data for multiple properties and calculates net profit or loss.

Which costs can landlords write off annually?

Mortgage interest, property taxes, insurance, maintenance, utilities, management fees, and travel expenses for property visits are deductible. Capital improvements must be depreciated over time.

How does property depreciation work for taxes?

Residential buildings depreciate over 27.5 years. Divide the property’s cost basis (purchase price minus land value) by 27.5 to determine annual deductions. Commercial assets use a 39-year schedule.

What’s the tax difference between repairs and upgrades?

Repairs (e.g., fixing leaks) are fully deductible in the current year. Upgrades (e.g., replacing a roof) are capital improvements depreciated over their useful life.

How do passive activity rules affect deductions?

Passive losses typically offset only passive income. However, actively participating landlords earning under 0,000 annually may deduct up to ,000 in losses against ordinary income.

What strategies lower annual tax bills for owners?

Maximize deductible expenses, defer taxes via 1031 exchanges, leverage cost segregation studies, and track state-specific credits. Consulting a CPA ensures compliance with local regulations.

Can cost segregation speed up depreciation claims?

Yes. This IRS-approved method identifies shorter-lived assets (e.g., appliances, flooring) within a property, allowing faster depreciation (5–15 years) and larger upfront deductions.

What records should property owners maintain?

Keep lease agreements, receipts, bank statements, invoices, and depreciation schedules. Tools like QuickBooks or Stessa simplify tracking income, expenses, and tax documents.